Locked lesson.

About this lesson

Identify the differences between cash basis and accrual accounting

Exercise files

Download this lesson’s related exercise files.

5.01 Accounting Methods - Exercise.docx50.7 KB 5.01 Accounting Methods - Exercise Solution.docx

84.4 KB

Quick reference

Accounting Methods

There are two accounting methods: cash basis and accrual basis.

Cash Basis

This is the most common method for small businesses.

- Income is recorded when the funds are received

- Expenses are recorded when the funds are paid

Accrual Basis

This is common among larger businesses and those that want to be able to see information in real-time. This is because it shows the financial impact of sales and expenses as they happen.

- Income is recorded when it’s earned

- Expenses are recorded when they’re incurred

Income Example

Services are performed and invoiced to a customer in April. The payment is received by the business in May. If the records are on a cash basis, the income is recorded in May. If the records on an accrual basis, the income is recorded in April.

Journal Entry Tip

- On a cash basis, the debit is the bank account.

- On an accrual basis, the debit is accounts receivable

- 00:04 Accounting Methods, how are the financial reports prepared?

- 00:09 When I say accounting methods, you might wonder, what does that mean?

- 00:13 There are two accounting methods, cash and accrual.

- 00:17 These are the methods used to determine how reports are generated and presented.

- 00:22 Let me explain what that really means.

- 00:25 The first method I'm going to explain is the cash basis method.

- 00:29 This is going to be the most common method for small businesses in the US.

- 00:34 It's very simple and easy for business owners to work with.

- 00:38 Income is recorded when the funds are received, and

- 00:41 expenses are recorded when the funds are paid.

- 00:45 The other method is an accrual basis.

- 00:48 This method is common among larger businesses, and

- 00:51 those businesses that want to see information in real time.

- 00:55 I'll explain.

- 00:56 Income is recorded when it's earned, so it doesn't matter when it's received,

- 01:01 expenses are recorded when they're incurred, not when they're paid.

- 01:06 I think it's going to make more sense if I show you some examples, so

- 01:10 we'll start with income.

- 01:12 Services are performed and invoiced to the customer in April,

- 01:16 the payment is received by the business in May.

- 01:19 If the business tracks their records on a cash basis,

- 01:22 the income will be recorded in May because that's when the payment was received.

- 01:28 If the business tracks their records on an accrual basis, the income will be recorded

- 01:33 in April, because that's when the services were performed.

- 01:37 I'm going to show you journal entries, not because I expect you to learn journal

- 01:42 entries, but because I want you to see in action what's happening behind the scenes.

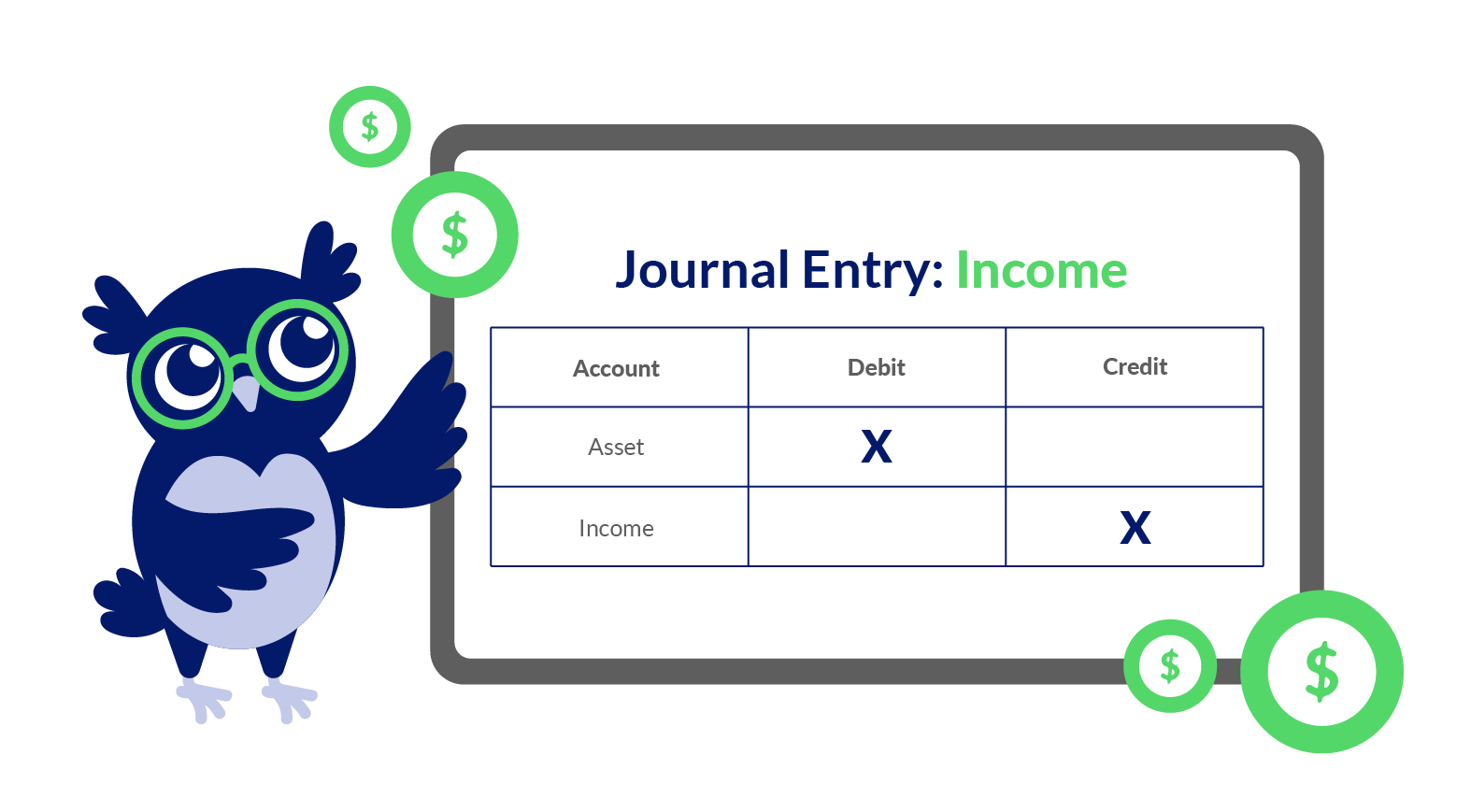

- 01:48 So when we look at income on a cash basis, we are going to debit or increase

- 01:53 the bank account, and we are going to credit or increase the sales account.

- 01:58 When a business tracks their income on an accrual basis, they will debit or

- 02:03 increase accounts receivable, and they will credit or increase the sales.

- 02:08 When the money comes in, they will debit or increase the bank account,

- 02:12 and they will credit or decrease accounts receivable.

- 02:17 Behind the scenes, what's happening is the accounts receivable cancels each other out

- 02:21 when the payment comes in.

- 02:24 What if the customer never pays?

- 02:26 On a cash basis there is no such thing as bad debt,

- 02:29 because on a cash basis no income is recorded.

- 02:33 The income on a cash basis is only recorded when the money comes in.

- 02:38 On an accrual basis, the bad debt is recorded when

- 02:42 the business determines the funds will not be collected.

- 02:46 But let's look at the journal entry for bad debt.

- 02:49 The bad debt journal entry only applies to accrual basis.

- 02:53 The first entry I have is to remind you when there is income,

- 02:57 it's a debit to accounts receivable and a credit to sales.

- 03:01 When there is bad debt, it is a debit to the bad debt account and

- 03:05 a credit to accounts receivable.

- 03:09 The idea is that you cancel out the accounts receivable, so

- 03:12 there's no longer a balance outstanding.

- 03:15 There's no longer a record that says the company is awaiting for

- 03:18 the customer to pay their outstanding invoice.

- 03:21 Let's move on to expenses.

- 03:24 Products are purchased and billed to the business in April.

- 03:27 The business pays for those products in May.

- 03:30 On a cash basis the expense will be recorded in May, because on a cash basis

- 03:35 you record when the money comes into or out of the account.

- 03:40 On an accrual basis, the expense will be recorded in April because that's when

- 03:44 the products are purchased.

- 03:46 Let's look at the journal entry for expenses.

- 03:49 On a cash basis, the debit will be the expense account, and

- 03:52 the credit will be the payment account.

- 03:55 The payment account could be the checking account or perhaps the credit card.

- 04:00 On an accrual basis, the debit is the expense account, and

- 04:03 the credit is the accounts payable.

- 04:07 When the payment is made, the debit will be accounts payable, and

- 04:10 the credit will be the payment account.

- 04:13 By doing this, accounts payable cancels each other out, meaning that there's

- 04:18 no longer a record of funds being owed to the provider of the products or services.

- 04:23 If you're wondering which method is best,

- 04:26 if there's a good one-size-fits-all, the answer it really depends.

- 04:31 There are so many nuances to accrual accounting, I simply put together

- 04:35 an overview to explain the differences between cash and accrual.

- 04:40 If you're in a situation where you're trying to decide which method is best,

- 04:44 my recommendation is to speak to an accounting professional familiar with

- 04:49 the particular business.

Lesson notes are only available for subscribers.